The $750K Property the Market Misread That Produced a 38% Return

A love letter to Yonkers' Nodine Hill

The best deals are most often where other people look least. During the pandemic, interest rates fell to such historically low levels that I had the opportunity to do a cash‑out refinance of one property to expand the portfolio. We originally planned to do a development project in Syracuse, NY, focusing on a live/work townhouse community, but the partner we planned on fell through. So, I was paying interest on a loan with no investment plan for the money. I spent nearly six months finding the right opportunity for a development project, but when it was time to make the hard commitments and sign on the dotted line, fear, uncertainty, and doubt caused one partner to withdraw. For some, even a project that takes on no debt is too much risk.

So, I found myself again at the crossroads of a critical decision. I couldn’t execute my original strategy without a partner, so I needed a new strategy. Given that our development projects are built around the unique attributes of each individual physical property, to execute this strategy again I would need to put in another six months of searching. Like all of my real estate career, I was actually working full‑time in a corporate environment. Since I had just landed a new gig, I decided to pivot to a new strategy that did not require as much searching, the cap rate vs. cost of debt arbitrage.

The cap rate vs. cost of debt arbitrage is fairly simple: if you can borrow all the money to buy a property at 4% and find a property with a 7% cap rate, you get 3% of the value of the property as annual cash flow. The twist in this scenario is that you are not borrowing the money for the new property by taking a mortgage on the new property; you borrow it all from the equity of another property. That’s exactly what we did. We were ready to be an all‑cash buyer at the depths of the pandemic.

Finding a 7% cap rate property anywhere near New York City is not easy. Investing in expensive neighborhoods where developers are looking to build million‑dollar condos means there is lots of speculative premium in the price. Those who invest in working‑class neighborhoods are operating properties for cash flow, not speculating on the next up‑and‑coming neighborhood. In 2021, that meant looking outside of NYC but close by. This strategy began to come together as we looked through hundreds of real estate listings within about a 250‑mile radius, from nearby Hoboken and Yonkers to the far‑away Lehigh Valley and Syracuse.

Using platforms like Zillow allows you to make a giant circle on a map, filter for multi‑family (since that’s my strategy), and sort the results by price (low to high). I would call this the “thrifting” strategy: look everywhere you would consider buying and see what the cheap stuff is. Why? Because we are not looking specifically for cheap properties; we are looking for inexpensive neighborhoods, there’s a big difference. We’re looking for places we may have never heard of or considered. In my case, I found Nodine Hill in Yonkers, NY. By 2021, I had lived and invested in Brooklyn for over 20 years, and I had never once even considered looking in Yonkers. In my mind, Yonkers was just a word I saw written in white letters on the green background of highway signs.

Once I started to find listings that met our investment criteria, we had another challenge: find a property where the cap rate is not a money pit of a building. You can always find “cheap” buildings; if the building is too rundown, it’s cheap now and expensive later. Nodine Hill is one of Yonkers’ oldest hilltop neighborhoods. Its name comes from the Nodine family, the landowners in the 1800s. As Yonkers industrialized along the Saw Mill River and Hudson waterfronts, workers moved uphill into neighborhoods like Nodine Hill, creating a dense, walkable residential district, just like my beloved home of Brooklyn.

Living in Nodine Hill gives you quick access to local highways, Yonkers public transit, a quick commute into NYC via Metro‑North, and rents at about 50% of NYC. Even better, Nodine Hill is right next to Yonkers’ downtown district for entertainment, nightlife, and culture. Nodine Hill fit into our strategic thesis of investing in places with deep community infrastructure: parks, public transit, schools, hospitals, and culture. Unfortunately, most of the buildings are old and in poor condition, our second strategic thesis. Poorly maintained neighborhood housing stock brings down prices. Some investors only care about the rent roll, ignoring the long‑term costs of maintenance. So, the best‑maintained and most expensive buildings don’t realize a market premium for their efforts. In reality, it is these properties that will be the cheapest buildings to own in the long term. The challenge: finding them.

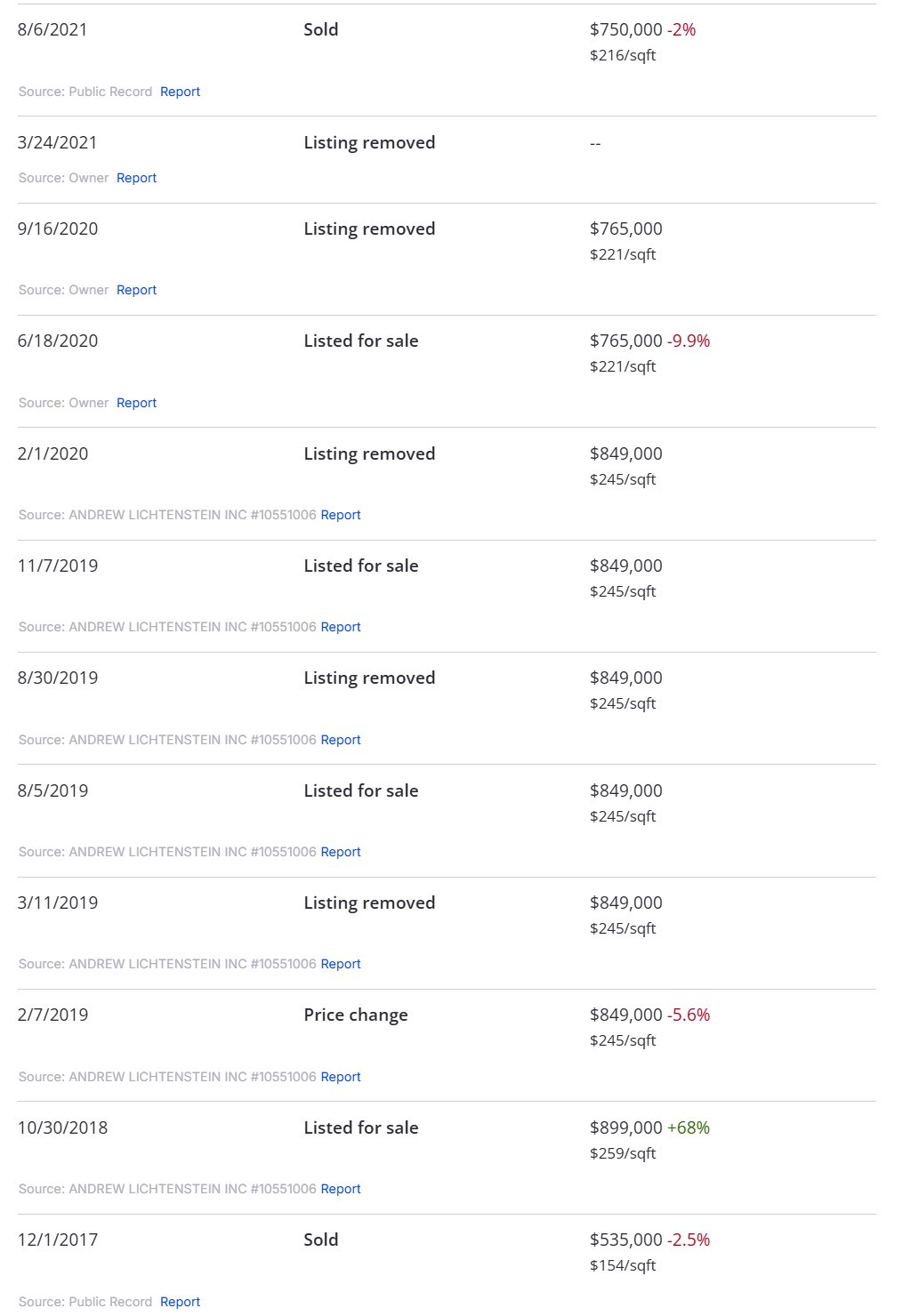

In a place like Nodine Hill, buildings with wildly different levels of disrepair, which could clearly be seen by a seasoned investor in the sale listing photos, were being offered at approximately the same price. Why? I don’t know. What I did know is that it was good for buyers, and at that moment, I was a buyer. I had stumbled across a listing with a very interesting history and promising interior photos. This property was listed for $899K in 2018 and had been on the market for nearly three years. The interior photos also looked like major work had been done.

The beauty of this listing was that the market had already done most of the hard part of negotiating the premium for me. Once I confirmed that this building was in outstanding condition relative to its neighbors, I knew this was a deal worth pursuing. The jump in the asking price seen between 2017 and 2018 was after the building was gut‑renovated. In reality, the building was physically much newer, but the new rents could not cover the premium in the asking price. That is precisely why this building sat on the market with three years of price reductions. This is a perfect target for an owner‑operator: great bones that you don’t have to pay for.

When you look at the price‑history chart, the opportunity jumps out immediately. This wasn’t a property rocketing upward with demand; it was a seller chasing the market down for almost three years. Listed at $899,000 in late 2018, then cut to $849,000, then dropped again to $765,000, and still unable to move. Multiple listings, multiple removals, and finally a sale at $750,000 in 2021. Sold a full $149,000 below the original ask, even as interest rates dropped by nearly 1.5%. That pattern tells you everything: buyers weren’t biting, the seller kept blinking first, and the market was quietly signaling that the price needed to come back to earth. Most people see a messy listing history and scroll past. I see a seller who’s already been softened up by the market and a deal that’s been sitting there waiting for someone who actually knows how to read these signals.

And this is exactly where an all‑cash offer becomes more than a tactic — it’s a lifeline. Remember what was happening during the worst part of the COVID epidemic. Sellers weren’t just tired; they were rattled. They had watched their listing sit through multiple price cuts, watched buyers disappear, watched the world shut down, and suddenly the idea of “holding out for the right offer” felt like a luxury from a different era. Every month the property sat was another month of uncertainty, another mortgage payment, another reminder that the market wasn’t listening to their original price. By the time I stepped in, this seller had been through three years of failed listings and a global crisis that made liquidity king. So, when I show up with a clean, all‑cash offer, I’m not negotiating against their asking price, I’m negotiating against their exhaustion. Cash‑in‑hand during COVID wasn’t just attractive; it was stabilizing. It was certainty in a moment when certainty was in short supply. And sellers in that headspace don’t haggle. They exhale. They take the deal. They want out, and cash is the fastest exit door in the building.

At the end of the day, this is why I don’t get hung up on the noise. The market had already done half the negotiating for me, the seller was worn down by years of failed listings and a pandemic that rewired everyone’s sense of risk, and the numbers made sense the moment you stripped away the emotion. We bought this building for $750,000 in 2021. Today Zillow values it at $925,000, which is a $175,000 gain on paper. The building has also produced about 3 percent free cash flow each year, which comes out to roughly $90,000 over four years. The depreciation schedule has created more than eighty‑seven thousand dollars in deductions, which translates into about twenty‑one thousand dollars in tax savings. When you add it all together, the total upside so far is roughly $286,000, and that is before any future rent growth or operational improvements.

But the truth is less glamorous than the headline number. Even with all our diligence, all our inspections, and all our modeling, we still had to replace a boiler for fifteen thousand dollars because in this business things break, surprises happen, and the spreadsheet never survives first contact with reality. That is the game. You buy right, you stay calm when something goes sideways, and you let time and competence do the heavy lifting.

Ready for more insights from the field? I’ve made the expensive mistakes, so you don’t have to. Subscribe to get weekly strategies, real numbers, and unfiltered lessons from 25+ years of actual deals. No theory, no fluff, just lessons learned and what actually works when your money is on the line.